Guy Foster, Chief Strategist, discusses the market movements of technology and energy stocks and bond yields. Plus, Janet Mui, Head of Market Analysis, analyses updated purchasing managers indices from the UK, U.S., and China.

The final week before the Easter break was a reasonably positive one for investors. The S&P 500 continued to reach new all-time highs and from a technical perspective there were encouraging signs.

For those concerned about the narrowness of the market earlier in the year, evidence of leadership shifting from technology and growth companies to a broader range of companies is good news.

Sometimes, technical analysis conflicts with fundamental analysis.

It’s encouraging to see broader participation in market gains, but amongst that increased breadth, energy stocks have been shining in recent weeks. Their strength reflects the return of some inflationary pressure from higher energy prices.

The oil price has risen into the mid $80s per barrel, close to its 2023 peak. The Organization of the Petroleum Exporting Countries (OPEC+) has maintained production cuts despite pressure from members to exploit reserves while demand remains high.

Energy stocks remain a valuable component of portfolios as companies are careful not to over invest, as was their tendency during previous cycles. This should enable the sector to maintain an unusual level of profitability. The energy sector also offers some benefits from a portfolio construction perspective because, as discussed above, energy price rises can be a problem for the economy and for growth equities.

So far in the first quarter, energy prices have contributed to a number of drivers of inflation, which the market has maintained a relaxed attitude to.

Last week, Federal Reserve board member Christopher Waller, who is known as a relatively hawkish member of the Federal Open Market Committee (FOMC), which sets interest rates in the U.S., explained that he sees the recent data on the economic outlook and the labour market to be showing continued strength. This, alongside slower progress in reducing inflation, persuades him that there should be no rush to reduce interest rates.

As it stands, the chance of a cut in June (the meeting after next) remains at a little over 50%, which seems surprisingly high based on current data.

How does Easter affect markets?

Last week was a shortened week for the UK due to the Good Friday bank holiday. The U.S. does not treat Good Friday as a federal holiday, but the stock market does remain closed on that day, by convention. Apart from the UK and U.S., several other markets were open despite strong Christian traditions leading to unusually thin trading.

Various trading strategies have determined there is both a Maundy Thursday and an Easter Monday effect, whereby these days exhibit above average gains relative to other markets. The general prevalence of markets to rise more often than they fall, and the tendency of price moves to be larger during times of lower liquidity, could explain these effects. However, these effects are less pronounced now that algorithmic trading, which doesn’t take holidays into account, has evened out some of the fluctuations in trading activity.

Easter has traditionally been a period of relatively benign markets with the more traumatic market events tending to be associated with September and October. However, it’s almost exactly 16 years ago that Bear Sterns was eventually rescued through its acquisition by JP Morgan, after seeing assets diminished by subprime mortgage exposure, an event eventually overshadowed by the failure of Lehman Brothers later that year.

The bunny and the bubble

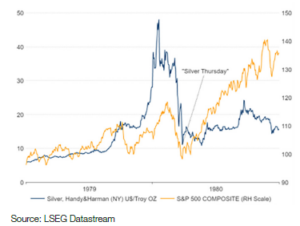

In 1980, Easter marked a tough time for the markets, which had suffered from fears of contagion effects as a speculative bubble in silver was unwound.

45 years ago, almost to the day, Silver Thursday occurred when three brothers (the Hunts) failed in their attempt to corner the silver market, believing the metal to be intrinsically under-valued as a hedge against inflation. Their aggressive accumulation of silver futures contracts sent prices up 500%. However, in response to apparent manipulation, regulators increased margin requirements, forcing the brothers to liquidate positions and resulting in an even sharper decline in prices with possible implications for financial stability.

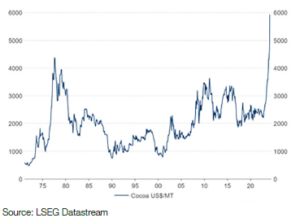

Today, cocoa is experiencing a sharp appreciation. Whilst it’s tempting to attribute this to Easter egg demand, it’s mainly a function of supply shortages due to low crop yields in West Africa, where weather conditions have been too dry. The rise in fertiliser costs driven by the war in Ukraine is also a factor. And yes, demand for chocolate has remained strong among consumers.

The direct impact on inflation will be modest, but it’s one more factor alongside the rise in energy prices, last week’s collapse of Baltimore’s Francis Scott Key Bridge, and continued harassment of shipping in the Red Sea, which has seen Suez Canal volumes down around 50% compared with the same period last year, according to the International Monetary Fund (IMF). These factors make it understandable that policymakers would be wary of easing monetary policy too fast and risking a resumption of the upward inflationary trend.