Guy Foster, Chief Strategist, discusses recent dovish interest rate announcements from central banks, while Janet Mui, Head of Market Analysis, analyses purchasing manager indices data from Europe and

the U.S.

Last week was big for central bank meetings. Although it saw the Bank of Japan (BoJ) raise interest rates for the first time in 17 years, the week was really characterised by dovishness from the central banks.

Interest rates rise in the East

European investors woke up to the BoJ’s decision last Tuesday morning. Money markets considered it touch and go whether it would hike or not, while consensus forecasts were firmly for the BoJ to keep rates in negative territory. However, news at the end of last week on the outcomes of the “Shunto” wage negotiations made the case for tightening much stronger. The Shunto translates to the spring wage offensive and represents a set season for wage negotiations, so if workers ended up striking together, their employers would not lose market share to peers. RENGO, the Japanese equivalent of the Trade Union Congress (TUC), announced last week that settlements achieved so far were above 5%; they were well below 4% last year. So, inflation by this measure remains strong in Japan.

Other measures seem less conclusive. Most obviously, Thursday’s inflation report would have encouraged the BoJ to tread slowly. Although headline inflation rose over the last year, that was mainly to do with fuel subsidies from last year dropping out of the numbers. The latest monthly inflation prints have been soft. The best measure, seasonally adjusted monthly moves in the core inflation rate, has been too low for the BoJ to hit its inflation target for the last four months. So, although the BoJ did technically surprise the market with an interest rate increase, its rhetoric was cautious enough to leave the outlook for further rate increases wide open. More people are talking about this being a one and done rate hike from the BoJ, although the money market still expects another two hikes this year.

Economic activity edging higher

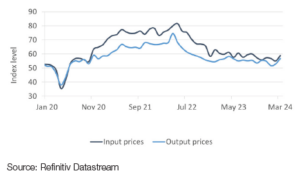

The most hawkish news for Japan came from Thursday’s purchasing managers indices (PMI). It showed the third consecutive expansion in activity overall, with services growing at the fastest pace in ten months, while the contraction in manufacturing was at its least severe since November. These data suggest demand is holding up in the economy. They also suggest that inflationary pressures remain, as output prices rose in both the manufacturing and services sectors, with higher raw material, fuel, transport, and staff costs being cited as the factors behind the increase.

Although the survey results suggest the above factors might be driving up Japanese prices, the fact that they are not evident in consumer price indices (CPI) suggests they could also be weighing on margins.

By contrast, the U.S. equivalent survey cited increased pricing power alongside “a steepening rise in costs”. This qualitative observation may tell us more about the disposition of the report author than the underlying economy, however, references to pricing power were notably absent from other regions.

U.S. composite PMIs input prices vs output prices

U.S. interest rates left unchanged

The Federal Reserve left interest rate policy unchanged on Wednesday. It acknowledged that the economy is doing better than anticipated, easing its growth and inflation forecasts for the year. But the Fed also left unchanged its expectation of three interest rate cuts. That was a slight surprise as CPI data has run hot and the consumer remains resilient. This doesn’t seem to have changed the outlook for rates much, but it has stalled the upward march of year-end U.S. interest rate expectations that have been underway since mid-January.

With Japan raising rates and the U.S. expecting to cut rates, you could be forgiven for expecting the yen to strengthen. It rallied a little in response to the Fed’s meeting, but overall ended the week lower. The reason for this is that while Japanese rates rose last week, the increase was marginal. The more important driver of the exchange rate is where each respective currency’s interest rates will be in the future, and in relative terms, U.S. expected rates have been rising relative to Japanese expected rates (Japanese rates rising less than expected, but U.S. interest rates being cut by less than expected).

The outlook for liquidity

A big focus for the year will be on the timing of the Fed’s exit from quantitative tightening (QT). It sounds from Fed speakers as if this could be announced at its next meeting. This could be a positive story for markets because QT was assumed to be a factor that would weigh on investor demand by reducing liquidity that might otherwise find its way into equity and bond markets. In fact, equity markets have performed admirably while quantitative tightening has been going on, and liquidity watchers put this down to the reduced use of the Federal Reserve’s repo facility.

Repo means repurchase agreement, and it allows an asset owner to raise short-term liquidity by selling an asset, such as a government bond, to another investor whilst agreeing to buy it back at a future date and price. In this way, it turns assets into liquid cash.

Reverse repo, as you might expect, is the opposite; specifically, it involves a central bank such as the Federal Reserve selling securities into the financial system but agreeing to buy them back later. For the duration of the agreement, the Fed will have taken the proceeds out of circulation. So, increasing use of reverse repo is a way of tightening monetary policy and vice versa. The reverse repo facility has been declining as banks have used it less, bolstering their own reserves and offsetting the impact from quantitative tightening. But that decline will need to slow, stop, or even reverse at some stage, which will have an impact on liquidity. The Fed is looking at how this can be coordinated with the more stimulative impact of reduced quantitative tightening.

Markets were strong last week as the Fed reiterated its three-cut guidance, but they have been strong in previous weeks even when that has seemed in doubt. This loose liquidity environment has been one of the explanations, and as the Fed experiments with the winding down of QT and less liquidity is released from the reverse repurchase facility, there will likely be some wobbles in the market. A particular sector to watch will be the U.S. regional banking sector because any shortfall in liquidity is likely to be reflected in declining bank reserves and a return of solvency worries due to the bond assets these banks hold, which currently stand at a loss.

The UK hawks take flight

The final (major) central bank reporting last week was the Bank of England (BoE). Again, there was no surprise about its decision to leave interest rates unchanged, but what did stand out was the change in voting, where two hawks had previously voted to raise interest rates but this time aligned with the majority to keep them on hold. Unlike in other regions, inflation has been declining slightly faster than expected in the UK. Much of this relates to the delayed impact of the utility bills cap, which meant that inflation seemed slower to take off, before being sharper, and lingering longer, after which it is now declining faster once more. Indeed, inflation is expected to drop to, or even below, the BoE’s target in the next couple of months as high monthly increases from a year ago drop out of the latest figures. But it is not expected to last, and despite the downside surprise to UK inflation last week, when looking beneath the surface, those indicators of persistent inflationary pressure remain. The median price increase, having been stable but still marginally too high for the last few months, lurched upward this month.

Some of this lingering inflationary pressure is good news. It reflects the resilience of the UK economy and the fact that the UK seems to be emerging from a cyclical downtrend, as reflected in the PMIs. In addition, as we discussed last week, the housing sector is improving both in terms of demand and construction activity. And, of course, there has been a two, soon to be four, percentage point reduction in tax on a substantial portion of the income for people with a high propensity to spend.

But some of the persistent inflationary pressure is down to a lack of productive capacity, partly explained by a high rate of economic inactivity, which itself is driven by an increase in long-term sickness. No doubt this will be one of the key dividing lines for policy going into the next election.