Markets fall post-Jackson Hole comments

Markets around the world fell last week following a crucial speech from Federal Reserve chairman Jerome Powell at the highly scrutinised Jackson Hole Symposium.

The falls were most severe in the US, where Powell’s hawkish speech caused the Dow to fall -2.36%, with the S&P 500 and Nasdaq also both falling -1.94% throughout the week.

Powell’s comments added to what had been a volatile week in Europe, where bad news around energy prices compounded the negative inflationary outlook. In the UK, the FTSE 100 fell -1.41% by Friday with the Stoxx Europe sliding -1.63 over the same period.

Falls were also recorded in Asian markets, though the picture there was mixed. While the Shanghai Composite index fell -1.27%, the Hang Seng posted a positive gain of 2.61%. This movement in Chinese equities was mostly led by an update on Friday that regulators were progressing in talks to avoid delisting in New York. Though the market was down, the losses seen in Japan’s Nikkei 225 were less than elsewhere in Asia – with the index down -0.53% by close of trading.

Last week’s market performance*

• FTSE 100: -1.41%

• S&P 500: -1.94%

• Dow: -2.36%

• Nasdaq: -1.94%

• Dax: -1.96%

• Hang Seng: 2.61%

• Shanghai Composite: -1.27%

• Nikkei 225: -0.53%

• STOXX Europe 600: -1.63%

*Data from close on Friday 19 August to close on Friday 26 August

‘Some pain’ comments cause falls

In his keynote speech at the annual Jackson Hole Economic Symposium, Powell bluntly warned that combatting inflation would likely “bring some pain to households and businesses”. He also told delegates the central bank would continue to use its tools “forcefully” to bring demand and supply back into balance. This all but confirmed the likelihood of further interest rate hikes for investors.

Markets fell immediately after the speech with the worst losses seen in the US. On Friday 26 August, the Dow Jones Industrial Average, S&P 500 and Nasdaq all fell 3.03%, 3.37%, and 3.94% respectively. The Dow Jones was the worst hit, down by over 1,000 points on Friday. Stock markets and bond yields had been rising in anticipation of the speech, but the hawkish tone and likelihood of further rate hikes has raised concerns over the US slipping into recession.

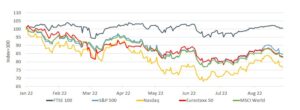

Global equity indices (rebased level)

Source: Refinitiv Datastream.

When markets reopened on Monday 29 August, losses were still being seen.

In Asia, the Nikkei 225 closed 2.7% lower by the end of the day with the Hang Seng index in Hong Kong also down 0.8%. This sentiment was the same in the US by the time markets opened – by the close of trading, the S&P 500 and Nasdaq had slipped 0.67% and 1.02% respectively.

China crisis looms

Signs of a looming property crisis in China became more apparent last week raising fresh concerns around the stability of the world’s second-largest economy.

On Thursday, Chinese premier Li Keqiang announced a package of support policies for the nation’s economy including a stimulus worth 1 trillion yuan ($146bn). Data in recent weeks indicates slowing Chinese economic growth, underpinned by falling house sales, which recently forced the country’s central bank into an unexpected rate rise.

The Chinese government also dispatched inspectors to 19 provinces around the country to gauge where further support can be offered. A stalling property industry has been identified as a critical issue for the economy, with construction projects halting and causing property prices to plummet.

On 30 August, Country Garden Holdings – China’s largest property developer – announced a 96% fall in profits and blamed a “severe depression” in the country’s property market. All this has forced many economists to cut China’s growth prospects for 2023. A Bloomberg survey of economists showed consensus expectations of 2022 Chinese growth are now 3.5%, down from 3.9%, with forecasts also cut for 2023.

European consumer outlook worsens

Major UK and European indexes were also impacted by Powell’s speech, but a worsening energy crisis was also a source of negative sentiment. In both Continental Europe and the UK, higher energy prices continued to raise concerns among investors about the impact this will have on consumers.

In the UK, the cap on energy prices was again raised by the regulator. From October, this will rise from £1,971 to £3,549 an 80% rise for the average household, with energy bills forecast to hit an average of £7,600 a year in 2023.

Russia has also moved to cut off gas exports to mainland Europe, announcing an imminent three-day halt to supplying its largest pipeline running to Germany. Though ostensibly for maintenance reasons, many commentators are recognizing this as a sign of things to come with Russia widely expected to cut off gas exports in winter. This caused consumer confidence in Germany – the largest economy in Europe – to fall to -36.5 points, a record low according to research firm GfK.

This has forced the European Commission to step in. On 29 August, it was revealed emergency intervention measures were being prepared by the EU in addition to structural reforms for the power market. Nations such as Germany, Italy, and Austria have joined a collective push to decouple gas and electricity prices.

Concerns of a European recession have ratcheted higher. Shorts on the euro have now reached their highest level since the start of the pandemic in 2020.[zuperla_single_image image=”22728″]